Dan Sundheim: AI Is Arriving When We Need It Most

Guest: Dan Sundheim, Founder and CIO of D1 Capital Partners Source: Inside Dan Sundheim’s Bets on Anthropic, OpenAI, and SpaceX | Duration: 01:26:51 Full Transcript: Complete transcript with speaker identification

Introduction

Dan Sundheim founded D1 Capital Partners at age 40. Before that, he spent roughly 14 years at Viking Global, eventually overseeing more than 55% of Viking’s capital. D1 launched in 2018 and today manages approximately $20 billion, making it one of the rare hedge funds with deep simultaneous exposure to both public and private markets — with positions in SpaceX, OpenAI, and Anthropic.

This podcast was recorded in early 2026, shortly after Claude Code entered public consciousness, and at a moment when software stocks were being heavily sold off and AI investment theses were facing their first real stress test.

Highlights from this episode:

- Why he evaluated Dario Amodei the same way he would have evaluated Bezos through his 1997 shareholder letter

- LLMs as a Netflix-plus-Spotify hybrid — personalization, not model quality, will be the lasting moat

- Hyperscaler moats are being systematically eroded by LLM customer concentration — a view Dan formed about a year before this recording

The Logic Behind a $20B Dual-Market Strategy

For most hedge funds, public and private markets are separate businesses requiring different teams, different rhythms, and different valuation frameworks. D1 chose to do both simultaneously, and believes there is genuine informational synergy between the two.

“So much of the innovation happening in AI is happening in private markets. If you’re going to have a view on AI companies in the public markets, you should have a view on where this technology is now and where it’s going. And investing in those companies gives you that perspective — it’s the strongest synergy I’ve seen in my career.”

Dan’s observation is that the competitive structure in private markets is entirely different from public markets. Private markets have fewer participants, but all of them are doing the same thing — analyzing company fundamentals and deciding whether to invest. Public markets have far more participants, but they are not playing the same game: some are quant, some are passive, some are event-driven, and fundamental long-term investors are actually a minority.

In private markets, there’s an interesting dynamic: fewer competitors doesn’t mean it’s easy to buy into the companies you want. The portfolio companies themselves have a choice — they need to actively want you as an investor. This gives firms that can provide genuine value to startups an additional competitive barrier; capital alone isn’t enough, you also need network and reputation. D1’s private portfolio (SpaceX, OpenAI, Anthropic, Ramp, etc.) functions as a credential, helping them gain access to the next company they want to enter.

This structural difference means holding Anthropic and SpaceX in private markets is not just about financial returns — it’s about information accumulation. Deep engagement with these companies gives Dan a cleaner picture of AI-related public market companies than purely public-market investors can develop. He noted in the interview that in D1’s early days, the public-private synergy was meaningful perhaps 25% of the time; in the AI era, that proportion has risen sharply — nearly every public market judgment benefits from having a private AI company vantage point.

At the current moment, late-stage private markets represent a particularly attractive opportunity in Dan’s view — some of the most valuable companies in the world remain private, and they are innovating in world-changing ways. This has never happened before: the most transformative companies on earth, at the most critical stage of their growth, are unlisted, leaving the vast majority of public market investors entirely without that dimension of information.

Reading Dario’s Writing the Way You’d Read Bezos’s 1997 Letter

Anthropic was not an obvious investment opportunity in its early days.

Several people Dan respects told him: investing in Anthropic is like investing in Lyft — backing the number two in a winner-take-all market, which is usually not “the path to glory.” He understood the analogy, but he had a different evaluative framework.

“At that stage, it was extremely hard to say who was first and who was second. What I was focused on was: can they become one of the long-term important players?”

The way he identified Dario Amodei, Dan says, is the same framework he would have used to identify Bezos.

Looking back on his career, one of his greatest regrets is missing Amazon early. If you only looked at the financial statements at the time, all you saw was losses — no financial signal at all. But if you had read Bezos’s 1997 shareholder letter — a document that articulated the company’s vision, value creation logic, and long-term goals with more clarity than virtually any other public company CEO he had ever seen — that was the real signal.

Dario gave him the same feeling. Not because Anthropic’s models were dramatically superior at the time (the technical gap between the major LLM companies was not large back then), but because of the precision of Dario’s writing and the depth of his focus:

“Writing things down forces you to really think everything through, and then express it in a way anyone can understand. Dario does that better than any CEO I’ve seen since Bezos.”

The logic for OpenAI was slightly different. D1 participated in an OpenAI funding round (Dan mentioned participating at a valuation in the $12.5 billion range), at a time when there was genuine debate in the market about whether LLMs were viable as a business model. Dan’s reasoning: uncertainty does not equal a bad opportunity — if the bet works, the upside is enormous; if it doesn’t, the downside is a manageable asymmetric position.

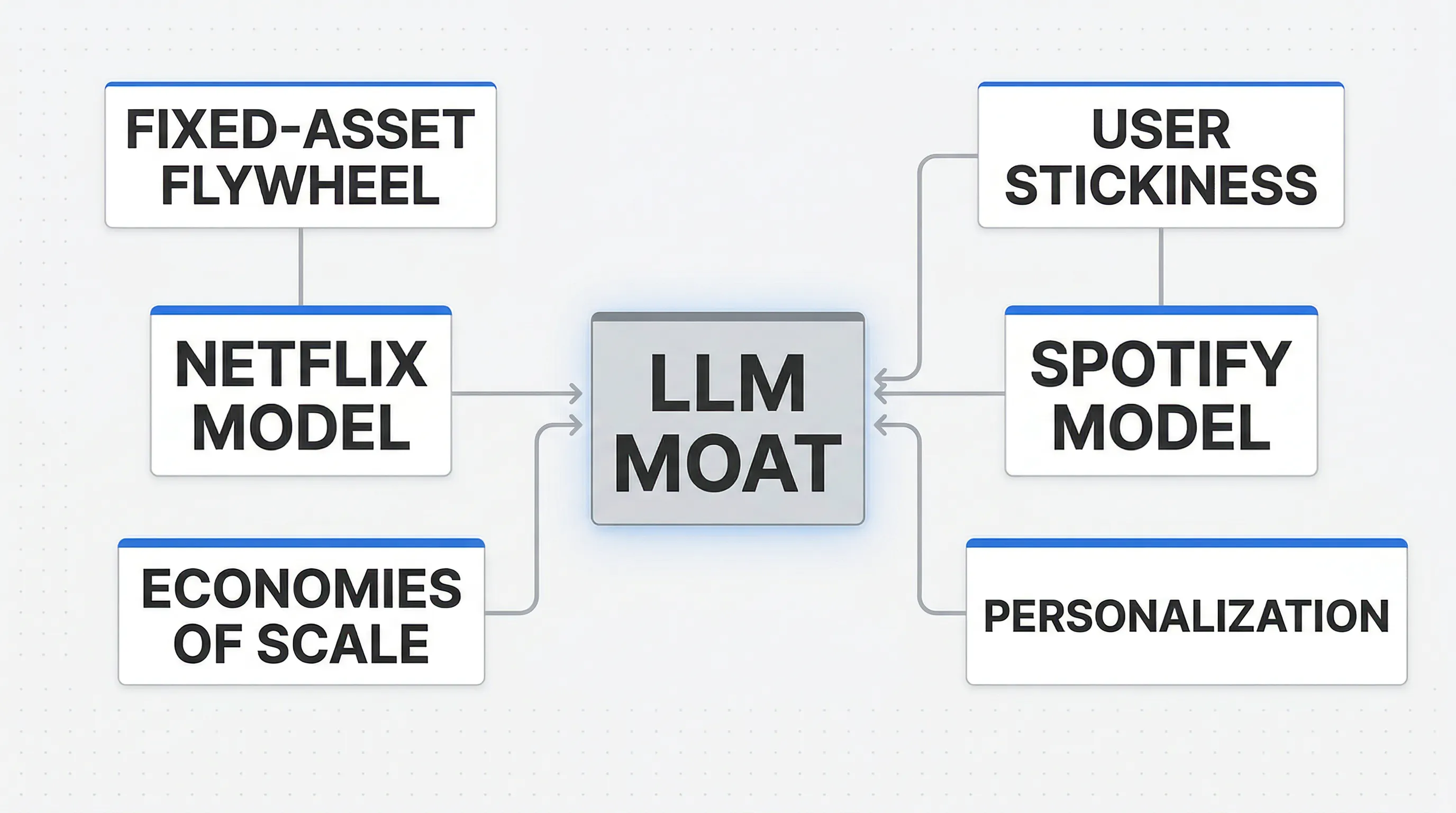

LLMs as a Netflix-Plus-Spotify Hybrid

How do you framework a business that has no precedent? Dan’s approach is to decompose analogies.

In conversations with executives at multiple LLM companies, he proposed what he considers the closest reference point: Netflix plus Spotify.

The Netflix part: Netflix invested large amounts upfront in fixed assets (content), but once that investment was made, the marginal cost of each additional sale was extremely low. The more you do this early, the more content you accumulate, the more users you attract, the more cash you have to invest in more content — it’s a flywheel, and the first-mover advantage compounds over time. LLM model training costs follow the same logic as Netflix content investment.

“You don’t know how much revenue this fixed asset will generate, but once it’s built, you want to sell it to as many people as possible so you can generate the cash to build the next model.”

But Netflix content is differentiated, while the quality gap between LLM models is narrowing rapidly — at one point OpenAI leads, the next Anthropic leads, but technological innovation diffuses quickly and gaps don’t persist. This brings in the Spotify part:

The music on Spotify is essentially identical in content to Apple Music or Amazon Music. So why does Spotify have pricing power? Why do users not want to leave? The answer is personalization — Spotify turned a commodity into an experience tailored specifically for you.

The ultimate moat for LLMs, Dan argues, is in the same place: whoever accumulates the most personalized user history first will be the hardest to replace. This has little to do with the quality of the underlying model, and everything to do with whether users are willing to start from scratch with a new provider.

The implication of this framework: the competition today is not just about model quality — it’s a race to accumulate user relationships.

Focus or Multi-Front?

The fact that D1 holds both OpenAI and Anthropic already signals that Dan is neutral on the core strategic debate between the two companies — he is more interested in watching how both paths evolve.

His view: Anthropic’s decision to focus on the enterprise was the right call at this moment. Abandoning the consumer side to go all-in on enterprise coding has given them market leadership. OpenAI’s multi-front approach (hardware, robotics, consumer, enterprise, science) is harder, but if any company can pull it off, it might be OpenAI — because the people who can work there are among the best in the world.

One early piece of advice that has been proven right: Dan told OpenAI about a year and a half ago that “you have to do advertising.” Silicon Valley has an instinctive aversion to advertising — Reed Hastings said Netflix would “never do ads” while he was running the company. But economic logic ultimately wins. If you’re going to do it eventually, doing it earlier and building the corresponding culture sooner gives you an advantage. OpenAI moving toward advertising now is a bit late on timing, in Dan’s view, but the outcome should still be right.

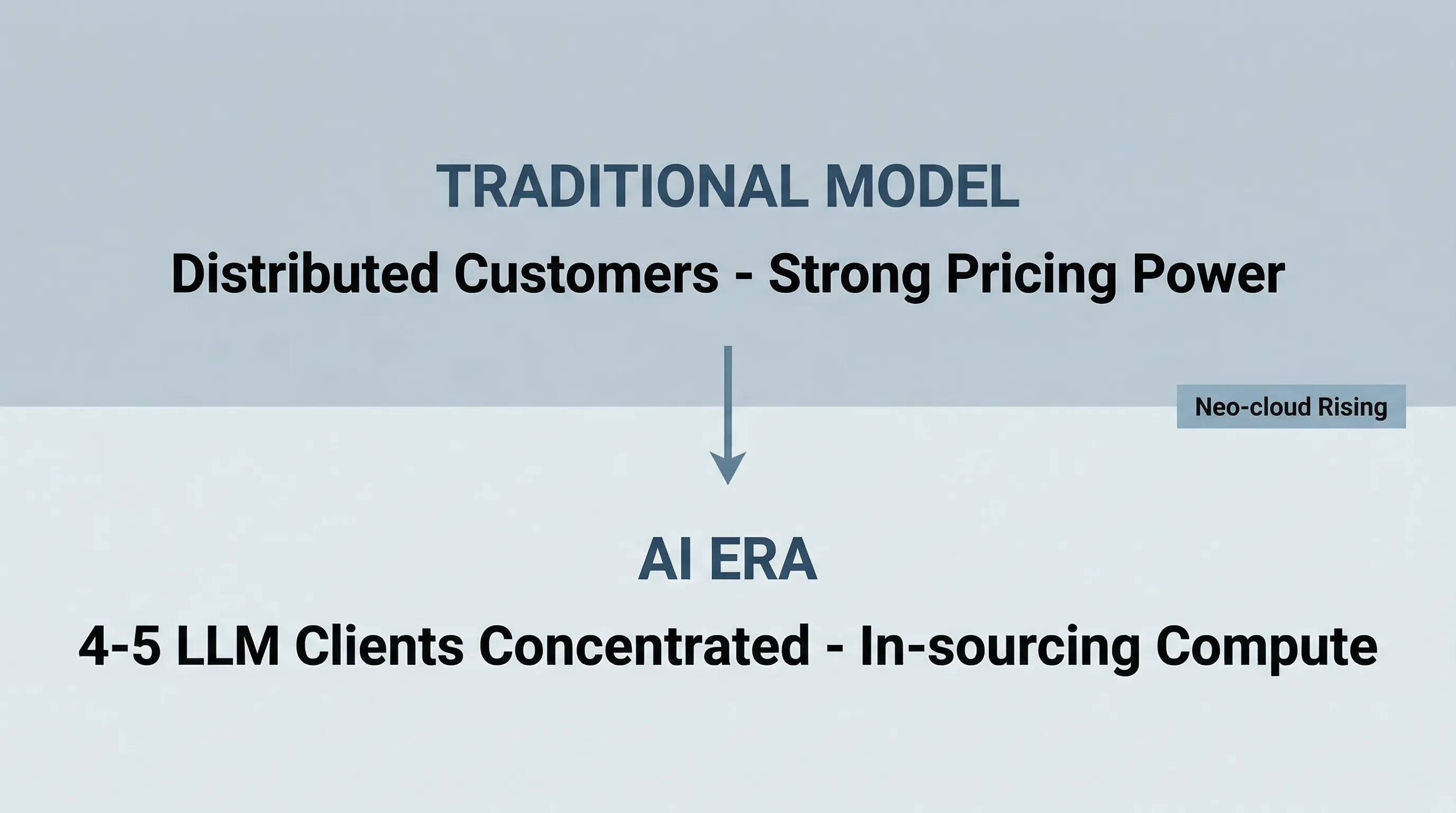

Hyperscalers: A Worse Business

This is one of the most direct and valuable judgments in the interview.

“I’ve been thinking about this thesis for about a year. I’m not saying it’s a certainty, but I’m more confident now — hyperscalers as a business are getting worse.”

The counterintuitive part of this view: he does not believe AWS or Azure revenues will decline — in fact, he thinks the near-term trajectory will accelerate (because OpenAI, Anthropic, and similar large customers are expanding rapidly). But “getting worse” refers to moat erosion.

The traditional hyperscaler moat was built on extreme customer fragmentation: every company in the world is a potential customer, no single customer is large enough to threaten pricing power, and AWS’s scale economics are unmatched.

The AI era has changed this structure:

- AI workloads are concentrating in 4-5 LLM companies, and these companies are becoming hyperscalers’ most important customer segment

- As these companies transition from cash-burning today to generating substantial free cash flow in 5-10 years, they have no economic reason to continue outsourcing their compute

- LLMs are actually better at GPU inference than traditional hyperscalers, whose advantage is in CPU clusters, not GPU clusters

- Neo-clouds (GPU-focused cloud providers) are rising, with Nvidia actively supporting their existence as an independent customer base to prevent compute markets from being monopolized by legacy hyperscalers

Meta is the precedent — as a company large enough to self-build, it has already fully internalized its compute. Over the next decade, AI workloads will represent a growing share of all hyperscaler activity, and the LLM companies supplying those workloads will ultimately make the same judgment.

At the same time, Dan believes the software industry is facing AI’s first real wave of disruption. After Claude Code entered public consciousness, markets quickly sold software stocks heavily, with the logic being: if a CRM can be vibe-coded in a day, what exactly is the legacy software company selling?

His view: what software companies face is something like what Walmart faced with e-commerce — painful, but if you have good distribution networks and system-of-record status, you can survive and even emerge stronger. System-of-record software (ERP, CRM) is relatively safe for now, because no one is going to run their entire enterprise backend on production vibe coding. But no software company can rest easy just by claiming “I’m a system of record” — all of them need to proactively integrate AI.

SpaceX Was Right, Rivian Wasn’t

Around 2019, Dan wrote large checks to both SpaceX and Rivian in roughly the same period. The two investments ended up worlds apart.

The Rivian thesis: EVs are like the iPhone versus Nokia — a pure hardware company cannot transform into a software company. EVs will dominate the auto market, and Rivian was one of the few with a real shot at being a winner. The thesis itself wasn’t obviously wrong, but the manufacturing ramp went sideways — the cash burn far exceeded expectations, and scale economies were slow to materialize. “The bad news arrived faster; the good news needed more time.”

The SpaceX thesis: engineering achievement is the valuation logic.

“From an engineering standpoint, SpaceX has accomplished the most stunning feats I’ve ever seen. If I can buy a company at some revenue multiple that barely burns cash, and that company has already demonstrated this level of capability — I don’t need to know what they’re going to do next. That alone is enough.”

Starship’s success exceeded his expectations. Once full reusability is achieved, launch costs will drop dramatically, which redefines Starlink’s TAM from “covering remote areas” to the entire global telecommunications market.

He also noted a general rule of private market investing: failed investments tend to show up faster, while great investments take longer to materialize — because excellent founders keep making new decisions, each one changing the trajectory, and that compounding effect takes time to accumulate.

GameStop’s Lowest Point — He Chose to Host an LP Dinner

In January 2021, the GameStop event hit D1 hard — taking them from the top of the industry to outside speculation about whether the firm might close, something Dan had never experienced in his 20-plus-year career.

By May-June 2022, D1 was at the trough of its largest-ever drawdown. Company president Jeremy suggested canceling the scheduled semi-annual LP dinner — “it’s going to be a bloodbath.” Dan’s decision: we have to go.

“That is precisely the moment when you need to face your investors.”

The message at the dinner was not a defense of past performance, but an announcement of change: the future portfolio would be built more conservatively — hitting singles and doubles, not swinging for home runs.

“That means it’ll take longer to get back to the high-water mark, because singles and doubles don’t produce fireworks. But what we went through in ‘21-‘22 taught me that even if taking high risk is theoretically the correct NPV decision, emotionally I cannot go through that again.”

He described a psychological shift that happens during a crisis: when things are at their worst, there’s nothing you can do, and that helplessness is the hardest part. But once there’s a plan — even if the outside world still doubts it — and the internal team believes in it, the sense of agency comes back.

Some investors redeemed from D1 after GameStop. Dan says he understood, and harbors no resentment: “Capital follows returns. Our returns were bad. It was right for capital to leave.” The LPs who stayed, he says, have his genuine gratitude — not as a courtesy, but because he believes the people who stay with you through the hardest moments are fundamentally different from the ones who gather around you in good times. This is consistent with his broader view on loyalty: most of his core team are people who have followed him for years, some of whom he knew before he had money. Jeremy is a childhood friend who is now company president. “People you meet after you’ve achieved success — you can never be quite sure whether they’re there for you or for what you can give them.”

Short Selling Is an Investor’s Best Friend

Shortly before GameStop, Dan spoke about his enthusiasm for short selling — something that feels somewhat out of place in today’s hedge fund landscape.

Markets are becoming structurally less efficient, not because there is less information, but because the composition of participants is changing. Twenty or thirty years ago, the dominant force in public markets was active management funds — investors broadly anchored to fundamental long-term value. Today, passive capital, retail investors, and quantitative multi-managers have become significant market forces, and even the quant multi-managers who look at fundamentals tend to be short-term in orientation.

The result: short-term price deviations from intrinsic value are wider today than they used to be.

“My wife begs me every time she sees me to stop shorting. But most people in this market aren’t investing on fundamentals — which naturally creates endless short opportunities.”

Social media and retail platforms like Robinhood have amplified this effect further, making narrative-driven price swings more extreme. Fundamental investors, as a minority, actually have larger structural advantages in this broken market — including on the short side.

In the AI era, this logic has a new application. Dan wrote in D1’s investor letter that before 2026, there were virtually no obvious short candidates in AI — anyone trying to profit by shorting AI victims probably lost money. But starting in 2026, as AI’s impact moves from narrative to reality, large numbers of companies worth shorting will emerge, with software being the first. This emergence of short candidates also provides a hedge for long AI infrastructure positions — in his framework, this is a genuine pair-trade logic.

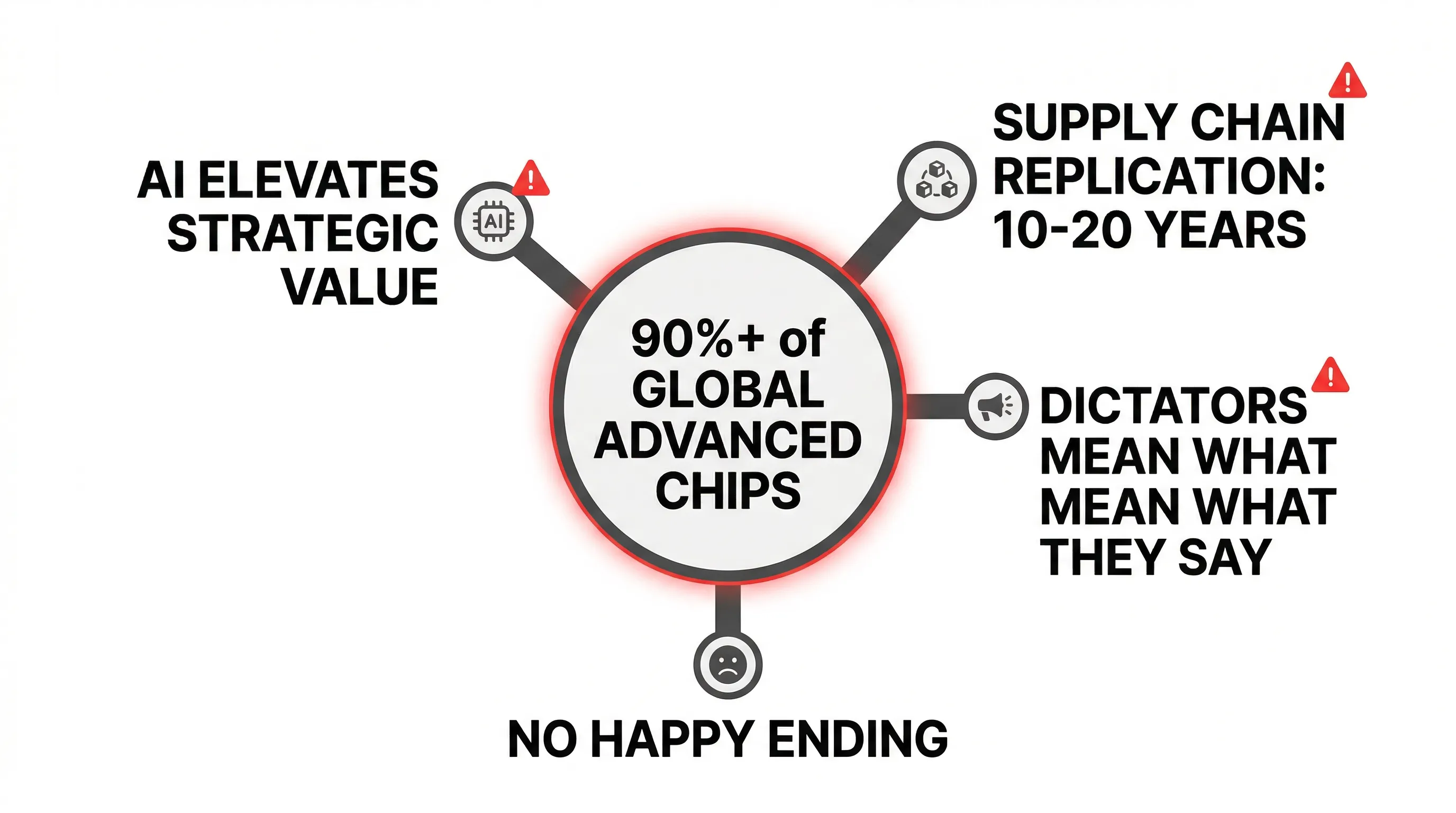

Taiwan Semiconductors: No Happy Ending

Near the end of the interview, Dan raised what he considers the most serious systemic risk worth worrying about today.

Taiwan produces more than 90% of the world’s most advanced semiconductors. Every product dependent on chips — phones, cars, servers, weapons systems — depends on this supply chain. If that chain is severed or forcibly interrupted, Dan believes the outcome would be “in the range of the Great Depression.”

“I can’t find a single scenario where everyone is happy. It’s not that there are no viable paths — it’s that every path has someone paying a price.”

He thinks the most plausible path is: the United States spends 10-20 years replicating semiconductor supply chains domestically, while during that period reaching some tacit understanding with China — one that gives China a visible long-term path to “reunifying Taiwan,” in exchange for temporary acceptance of the status quo.

But this path contains its own paradox: once the United States completes supply chain replication and reduces its defensive incentive to protect Taiwan, China may actually accelerate action.

He invoked a rule about autocrats: take what autocrats say seriously. When Putin kept emphasizing the glory of the Soviet Union, he acted once he had the capability. Xi Jinping emphasizes Taiwan in every major address. The rise of AI has further increased the strategic value of semiconductors, and raised the economic damage potential of any conflict. This makes the risk more prominent over the next decade, not more distant.

Editorial Analysis

The Guest’s Position

Dan Sundheim’s positive statements about Anthropic, OpenAI, and SpaceX in this interview need to be understood against the backdrop of his being a direct investor in all three. D1 Capital holds substantial positions in these companies, and any comments that improve public confidence in them objectively benefit his portfolio. This doesn’t necessarily mean his judgments are wrong, but readers should be aware of this interest alignment.

Dan manages LP capital, and his business model depends on scale growth and strong performance. His optimistic forecasts about AI-driven economic growth are consistent with fund-raising logic — that doesn’t make them suspicious, but it is worth noting.

Selectivity in the Arguments

Rivian’s failure attribution: Dan attributes Rivian’s poor outcome to manufacturing ramp failure rather than to any flaw in the selection logic itself. But a more complete reflection would include: entering private market investments in capital-intensive manufacturing carries inherently different risks than investing in pure software companies — was the valuation at the time actually pricing in that uncertainty?

Blind spots in the hyperscaler critique: Dan’s argument assumes LLMs will fully internalize compute, citing Meta as the precedent. But Meta is an extraordinarily technology-oriented company that had already built massive self-run infrastructure long before the AI era. More importantly, Google/Alphabet is simultaneously a hyperscaler (GCP) and an LLM player (Gemini) — its internal structure is completely different from OpenAI or Anthropic — and this case is conspicuously absent from Dan’s framework.

The Other Side of the Argument

LLM switching costs are overstated: Dan’s Spotify personalization moat argument assumes users will develop deep stickiness with a particular LLM. But Spotify locks users in through years of accumulated listening history and algorithm tuning; LLM “personalization history” is technically much easier to migrate or rebuild, especially for enterprise users. The cost of switching APIs is far lower than rebuilding a music preference database.

Software company resilience is underestimated: Dan’s Walmart analogy for software companies adapting to AI isn’t quite right. Walmart faced external competition from Amazon; software companies are facing AI tools that lower the bar for users to build their own solutions — this is closer to “productivity tools that make users no longer need you” than “a better competitor appearing.” The two situations require different response strategies.

Fact Check

- “Taiwan produces 90%+ of the most advanced semiconductors”: Broadly accurate. TSMC’s market share in 3nm and below exceeds 90%, with other sources (Samsung, etc.) representing a minimal share.

- “D1 invested in OpenAI at a $125B valuation”: Dan mentioned this figure, but in OpenAI’s documented funding history, $125B corresponds to the October 2024 round led by Thrive Capital, not an early round. The timing may be conflated here; readers are advised to independently verify D1’s specific investment timing.

- “Anthropic considering building 10GW of its own power”: Dan said he “saw this piece of news,” but as of the interview date, it was unclear whether this had been officially confirmed.

Key Takeaways

Identifying great founders: look at the clarity of their writing over the quality of their current product. In the early stages when technology is not yet differentiated, the quality of a founder’s thinking is the most reliable leading indicator — Bezos’s 1997 letter is the precedent, Dario’s writing is the follow-on example.

The real competition among LLMs is the speed of accumulating personalized history, not the current gap in model quality. Whoever locks in user personalization data first will have a deepening moat — this is the core metric worth tracking.

Hyperscaler moats are eroding, but the time horizon is 5-10 years. Near-term growth continues; long-term marginal value is declining. For portfolios with AWS/Azure exposure, this is a risk worth factoring in early.

Taiwan semiconductor risk is not a low-probability event. It is a high-impact, medium-probability systemic risk, and the rise of AI has further amplified the strategic value of semiconductors, making this risk more prominent over the next decade, not more distant.

Based on Inside Dan Sundheim’s Bets on Anthropic, OpenAI, and SpaceX

If you found this helpful, consider buying me a coffee to support more content like this.

Buy me a coffee